While Retirement Researcher focuses on providing the education you’ll need to navigate your retirement planning journey and do-it-yourself, our sister firm, McLean Asset Management, serves as the implementation arm: done-for-you.

We understand that managing this process yourself is important to you, but we also know that retirement planning isn’t easy. And unfortunately, the reality is that you only get one chance to do it right. That’s why we have teamed up with McLean Asset Management to offer access to a one-time financial plan without the commitment of an ongoing wealth management advisory relationship.

Coming Soon: Retirement.

But getting help with my retirement requires a long-term commitment to an advisor?

So what is the Standalone Plan all about?

"Unbundling" Access to Retirement Planning Expertise

It's All About You

What is Included in a Standalone Plan?

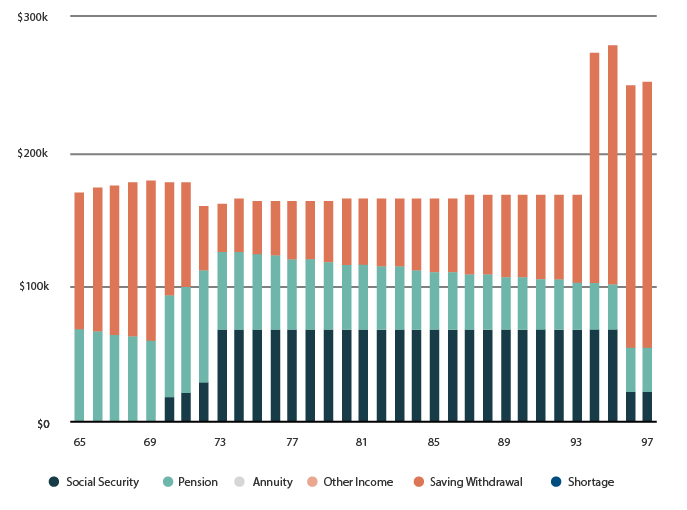

A Reliable Income Analysis

A Reliable Income Analysis Includes:

Spending Needs Analysis

A review of your spending needs, with recommendations for how to fund them. Includes recommendations for adjusting your funding sources to better align with your goals.

Income Flooring

An analysis of your planned income sources throughout retirement and how they can be optimized to fund expected expenses. We will identify your income floor and whether additional income is warranted based on your circumstances. If applicable, specific implementation recommendations will be provided.

Social Security Optimization Analysis

A review of potential claiming strategies available to optimize your Social Security income stream.

A Tool to Learn Your Retirement Income Preferences

Take the RISA® and learn your retirement income preferences.

There are many ways to construct a successful retirement income plan. There is no one-size-fits-all approach.

The best tools for your plan largely depend on your retirement income style preferences. The RISA® serves to evaluate your preferences, aligning them with specific implementation tools and strategies that align with your “profile.”

Think of it like a personality test for your retirement income preferences.

An Investment Review

A Tax Planning Review

McLean will review your prior year’s income tax return to identify tax planning opportunities.

The engagement also includes an analysis of your retirement income plan with recommendations for tax-efficient and tax-saving strategies such as asset location changes or Roth conversions where appropriate.

A tax projection will be provided that illustrates the potential impact of implementing tax planning recommendations.

An Insurance Review

McLean will review existing life insurance, annuity contracts, disability policies, and long-term care policies, recommending changes where appropriate. As part of your goals-based financial plan, McLean will evaluate your coverage needs and analyze whether insurance products can increase your plan’s probability of success, recommending specific products where appropriate. Note that there is no obligation to implement any insurance recommendations with McLean.

And Any Other Considerations

All Culminating In...

A Presentation of Goals-Based Financial Plan and Recommendations

If applicable, the following services will be included:

Pension Review

Medicare Election Consulting

Education Planning

Charitable Planning or Gifting Strategies

Is this just a sales pitch to gather my assets?

Is this just a sales pitch to gather my assets?

No! We believe in comprehensive planning and invest 40+ hours of professional time into each engagement.

Many firms that offer a “free” or low cost plan are often using it as a sales tool to gather assets. McLean designed a comprehensive engagement that covers the baseline needs for most people. Instead of a “bait and switch” tactic, we are simply charging for the time it takes to build the plan and present our recommendations.

Is this just a sales pitch to gather my assets?

The engagement begins with a Discovery meeting and talk through the specifics of your planning needs. After that meeting, the planning team gets to work building your personalized plan based on the information provided. Once the plan is ready, we will meet again to review the output, implementation recommendations, and next steps. There is an option to schedule a follow-up call to address questions for a period after the plan presentation meeting.

Meet your Team

Jason Rizkallah,

CFP®, RICP®, ChFC®

Alex Scott, CFP®, RICP®, ChFC®

Financial Planner

Lauren Squeglia, PPC®

Planning and Insurance Coordinator

Our standalone plan has a

standalone payment.

Makes sense.

One-time

payment:

$7,995

Annual

Academy Member

Discounted Price

$6,995

Questions?

Take the next step

towards retirement clarity.

's Syllabus

Retirement Income Challenge

Ongoing Investment Management Main Page